What is self-funded insurance?

Self-funded insurance, also called self-insured insurance or a self-funded health plan, is a funding arrangement in which the employer pays employee healthcare claims directly, rather than paying a fixed premium to an insurance carrier.

The employer sets aside funds to cover anticipated claims, partners with a third-party administrator (TPA) to process them, and purchases stop-loss insurance to cap financial exposure from large or unexpected claims.

Unlike a fully insured plan, unused dollars don’t go to an insurer at year end. They stay with the employer. And because the employer owns the claims data, they can see exactly what’s driving healthcare costs — and take action.

Self-funded vs fully insured

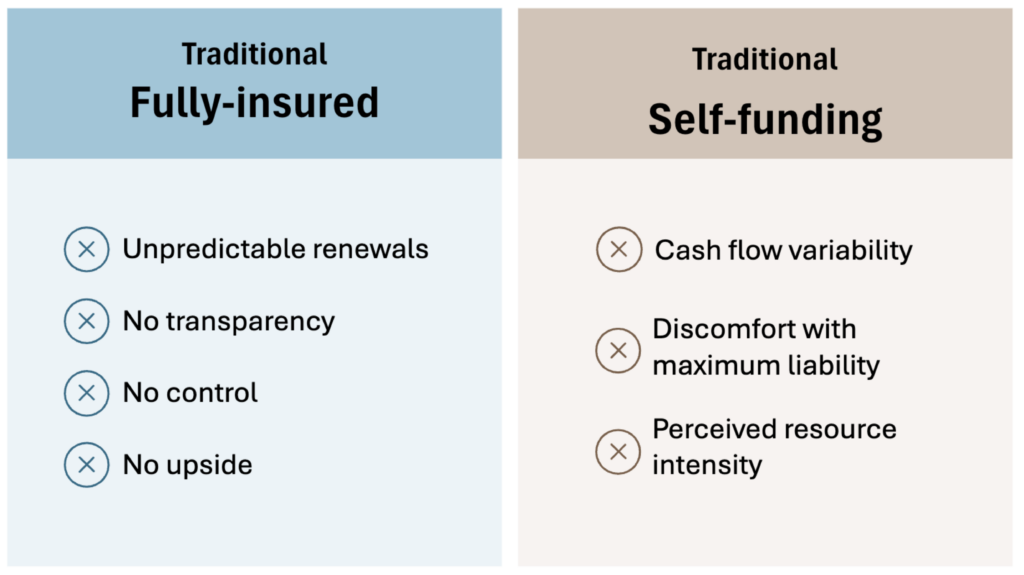

With a fully insured health plan, the employer pays a fixed premium to an insurance company. The insurer pools that money with other companies’ premiums, pays medical claims from that pot, and keeps whatever’s left over.

Because the insurer takes on the risk of paying large claims, they build in extra cushion to protect themselves. That’s why fully insured employers have high fixed costs. The employer is paying for the insurance company’s safety net and administrative inefficiency, not just the actual cost of healthcare.

In a self-funded health plan, employers set aside funds to pay claims directly, as they occur. This funding model provides the potential for healthcare cost savings because employers pay only for the healthcare their employees actually use. Additionally, self-funded employers have more levers to lower healthcare spend.

Watch this video for a deeper dive into self-funded vs fully insured.

How does a self-funded health insurance plan work?

Self-funded health insurance plans rely on three essential components:

-

Benefits administration

Third-party administrator (TPA) + pharmacy benefit manager (PBM)

A self-funded employer partners with a third-party administrator (TPA) to handle the medical side of the health plan. The TPA manages day-to-day operations:

-

-

- Processing medical claims

- Issuing ID cards

- Answering employee questions

- Managing provider networks and eligibility

-

On the prescription side, a pharmacy benefit manager (PBM) oversees pharmacy claims, determines which medications are covered (formulary management), and negotiates pricing with pharmacies and drug manufacturers.

-

Claims funding

Employers pay the actual cost of employee healthcare

Instead of paying fixed premiums to an insurer, self-funded employers pay for the actual cost of smaller medical and pharmacy claims. For example; doctor visits incurred by employees and their families.

-

Stop-loss insurance

Protection against large or unpredictable claims

Self-funded employers purchase stop-loss insurance coverage to cap their financial exposure to large unexpected claims.

Specific stop-loss insurance limits the cost of any single individual’s claims.

Aggregate stop-loss insurance limits the employer’s total claims liability across the entire population for the plan year.

Click here to learn how stop-loss insurance works.

Self-funding with a captive vs traditional self-funding

Self-funded health insurance plans work best as a long-term strategy. But traditional self-funding can expose small and midsize employers to volatility, especially with the rising size and frequency of catastrophic claims.

That’s what’s different about going self-funded with a ParetoHealth captive. ParetoHealth unites thousands of employers into one strong community that shares risk and uses scale to unlock industry-leading protections and savings.

By self-funding with a ParetoHealth captive, employers keep the upside of self-funding and gain the stability of scale. Instead of reacting to unpredictable annual premium increases, employers who self-fund with a ParetoHealth captive can focus on a long-term strategy to reduce healthcare costs.

The Self-Insurance Institute of America (SIIA) notes that employee benefits captives are now the fastest-growing self funding model among midsize employers.

What is a captive?

A group self-insurance arrangement owned by Members. Members pool resources to self-insure collectively. Pooling risk means that one Member’s high claims are offset by others’ with lower claims, reducing year-to-year cost volatility for all Members.

Because the captive is Member owned, profits (if any) from the risk pool are reinvested or returned to Members, creating added value beyond typical insurance. Losses are also shared by the Members.

What is an employee benefits captive?

An employee benefits captive is a captive owned by employers to manage and finance their employee benefit programs.

What is the difference between a P&C captive and employee benefits captive?

The main difference is the type of risk that each covers. A property and casualty captive (P&C captive) manages physical liability risk such as property, auto, or workers compensation. An employee benefit captive manages employee-related costs such as medical costs, disability, or life.

Some P&C captive companies may attempt to diversify with an employee benefits captive structured as an A/B fund model. The A fund is the individual captive layer and the B fund is a shared pool. The A/B fund model forces employers to pre-fund both individual and shared layers, plus post collateral, while leaving the employer exposed to as much as 150% of premium before stop-loss kicks in. Surplus returns aren’t guaranteed and the A/B fund model structure creates volatile renewals instead of true protection.

ParetoHealth avoids these pitfalls by eliminating unnecessary pre-funding, requiring less capital, and offering long-term contract protection with predictable renewals and comprehensive cost containment.

What are the advantages of self-funding with a ParetoHealth captive?

The advantages of self-funding with a ParetoHealth captive include our unmatched scale, the ParetoHealth Risk Shield, the ParetoHealth Savings Engine, data transparency, and the ParetoHealth community.

Unmatched scale

When you join ParetoHealth, you’re joining the largest and fastest-growing community of its kind. This scale unlocks risk protection and negotiation leverage that midsize employers can’t get on their own.

ParetoHealth Risk Shield

ParetoHealth’s Risk Shield offers the best protections on the market include a guarantee of no new lasers and a cap on rate increases. This eliminates healthcare cost volatility and makes costs predictable year over year.

ParetoHealth Savings Engine

ParetoHealth’s Savings Engine addresses the root causes of high-cost claims. Backed by data, analytics, and in-house clinical experts, the ParetoHealth Savings Engine delivers curated programs and multiyear strategies that lower costs over time.

Data transparency

When employers join a ParetoHealth captive, they gain access to claims data and pharmacy rebate transparency. As a result, they can see exactly where their healthcare dollars are going and address cost drivers directly.

The Pareto community

ParetoHealth brings midsize employers together to solve what they can’t solve alone—unpredictable, rising healthcare costs. As one like-minded community, Members share insights, attend exclusive strategy events, and benefit from collective savings, when one Member takes action to lower costs, every Member benefits.

Rethink what’s possible with ParetoHealth

Thousands of midsize employers have already left fully insured health plans behind to join the ParetoHealth community and the movement is only growing.

ParetoHealth consistently outperforms traditional insurance, empowering small and midsize employers with a long-term solution to eliminate volatility and lower overall healthcare spend.

A multiyear claims-based study found that employers who moved from fully insured plans to ParetoHealth reduced healthcare costs by 7.5% in the first year and by an additional 16.5% annually by year three.

Midsize employers don’t have to feel stuck in fully insured health plans. With ParetoHealth, employers are taking control of their healthcare spend.

Learn more about how an employee benefits captive works.

Sources: Self-Insurance Institute of America (SIIA). Employee Benefits Captives: A Growing Solution for Employer Health Plans. Self-Insurance Institute of America, Inc. (2024). https://www.siia.org